108% is the new NRR median

The mid-market B2B SaaS NRR median sits at 108%. If your 2026 plan benchmarks the business against 120%, you're running scenarios against a market the 2025 data no longer supports. The gap is 12 points wide and compounds across expansion math. It shows up in valuation multiples within two reporting cycles.

Boards still anchored to 120% NRR built their playbook in a different capital cycle. From 2017 to 2022, three conditions held NRR above 115% for most mid-market B2B SaaS. Cheap capital funded expansion plays, growth-at-all-costs budgets pushed seat counts, and per-seat pricing defaulted to expansion through up-sell. All three reversed by 2024.

We read NRR benchmarks the way diligence leads do, with an overlay for the Churn Tax we published last quarter. The 108% median is the floor of the conversation. The harder number is the effective NRR after the three Churn Tax layers compound, and the effective number sets a different valuation conversation.

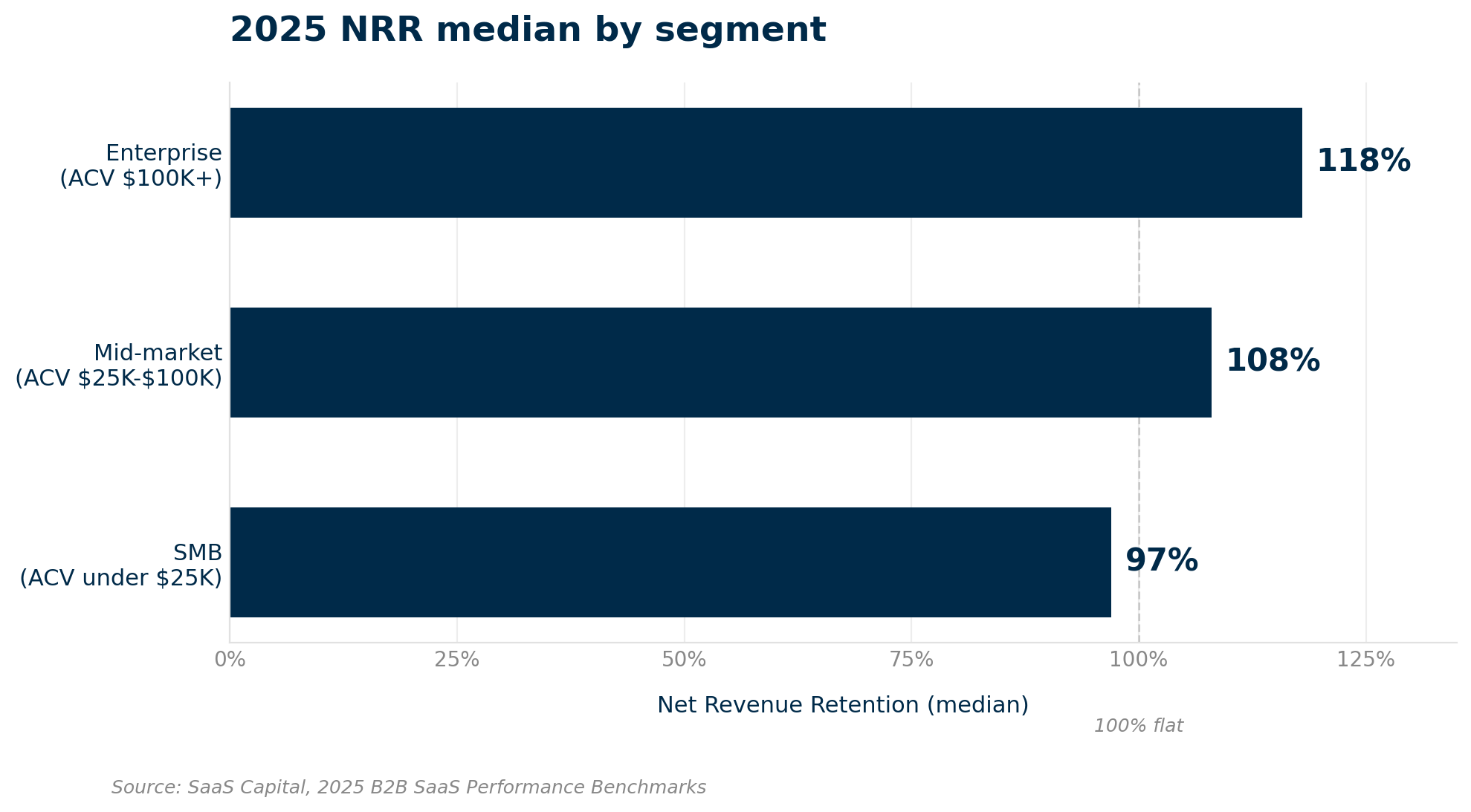

The 2025 segment tiers

SaaS Capital's 2025 dataset cuts the median by deal size, and the spread matters more than the headline.

Enterprise (ACV $100K+): 118% NRR median

Mid-market (ACV $25K-$100K): 108% NRR median

SMB (ACV under $25K): 97% NRR median

Three observations. Enterprise still expands, but the 118% number reflects a smaller cohort of survivors after the 2024 buyer-side renewal pressure documented in OnlyCFO's CFO mandate research. Mid-market is the new median anchor, SMB has crossed into contraction, with 97% reflecting downgrade pressure on seat-based pricing as buyer CFOs cut non-essential subscriptions.

If your portfolio company sits in mid-market and reports 108% NRR, the board narrative reads "in line with the market." Same 108%, but if the board still expects 118%, the narrative reads "underperforming."

The forces behind the move

Three forces compressed the NRR median between 2023 and 2025, and none of them are reversing.

Pricing model transitions. IDC reports 70% of software vendors are moving away from pure per-seat pricing by 2028. Hybrid pricing reached 61% by the end of 2025, with usage-based and consumption models leading the migration. Seat counts can't carry NRR the way they did from 2017 to 2022, and the expansion mechanic changes underneath. Companies adapting fastest see their NRR stabilize, while the ones still optimizing for seat upgrades see expansion flatten.

Buyer-side CFO pressure. OnlyCFO documented the renewal mechanics in May 2026. Buyer CFOs are introducing mandatory POCs, refusing multi-year terms, and adding aggressive opt-out clauses. Each compresses the renewal yield. Multiply across a customer base of 200 to 800 accounts, and the headline NRR drops two to four points in a single reporting cycle.

AI add-on revenue covers seat contraction. PwC's AI Software Valuations analysis flagged the diligence problem in early 2026. Companies are reporting healthy NRR because AI add-on revenue is offsetting seat contraction in the headline number. The NRR figure stays intact. The gross revenue retention figure tells a different story, and diligence leads are now pulling GRR alongside NRR before pricing the deal.

The Churn Tax overlay

The Churn Tax framework we published in March applies a 1.5x to 2.5x multiplier on reported churn to surface the effective revenue exposure. The three layers, lost recurring revenue, forfeited expansion, and replacement customer acquisition cost, compound across the customer cohort.

Apply the overlay to the new NRR baseline: A mid-market company reporting 8% churn and 108% NRR carries an effective Churn Tax exposure of roughly 20% of revenue once you aggregate the three layers. At $300M ARR, the exposure runs $60M a year. The headline 108% NRR doesn't surface this number, the diligence process should.

Once you apply the overlay, the board conversation changes. NRR functions as a partial signal alongside GRR, segment composition, expansion mix, and the Churn Tax multiplier. Anchoring the board narrative on a single headline number is how leaders get caught short at the next quarterly review.

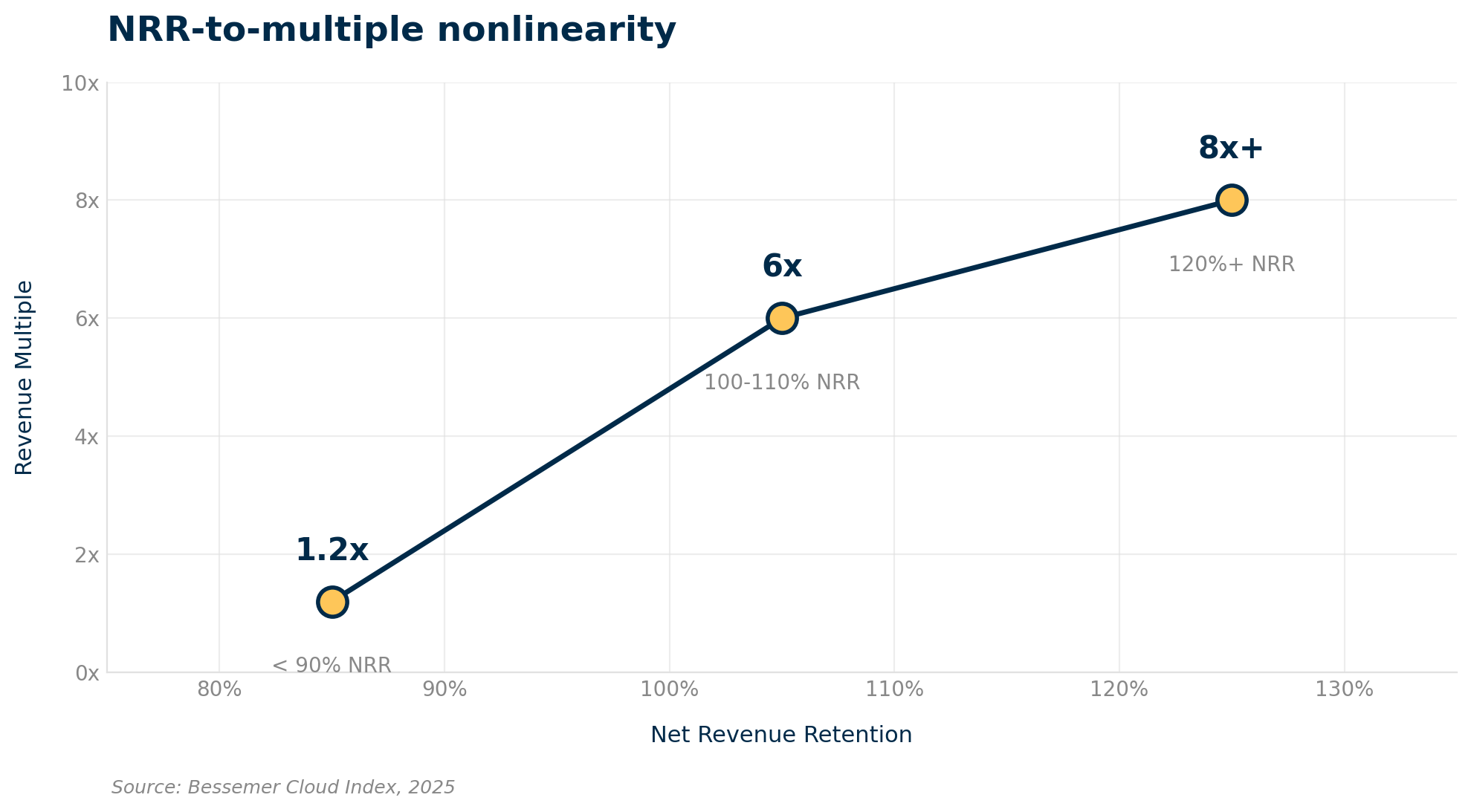

The valuation gap

McKinsey's NRR Advantage study tracked 100 B2B SaaS companies across a five-year window. The companies in the top NRR quartile traded at a 24x revenue multiple. Companies in the bottom quartile traded at 5x. NRR drives the 19x spread.

Each point of NRR carries nonlinear value: the Bessemer Cloud Index segmentation shows the curve:

Sub-90% NRR trades at 1.2x revenue

100% to 110% trades at 6x

120%+ trades at 8x and above

Moving from 108% to 115% is worth more than the linear math suggests because the multiple expansion isn't linear at the bracket boundaries.

Three moves for 2026 boards

Rebenchmark the plan to 108% as the mid-market floor, with segment-specific overlays. If your business is mid-market by ACV, the 108% number is the credibility-tested median. Anchoring above 108% requires a sourced rationale, like a verticalized SaaS comp set or enterprise-heavy ACV mix.

Report NRR and GRR together. The two numbers in tandem give diligence leads and boards the full picture they want, in an AI add-on revenue environment where NRR alone masks too much.

Apply the Churn Tax multiplier to surface effective exposure, the 1.5x to 2.5x range turns reported churn into capital allocation conversation. The conversation shifts from CS operations to revenue protection at scale.

The path forward

The benchmark reset is the easy part, the harder work is the operating model rebuild underneath. From a 108% floor, 2 to 3 points of NRR improvement inside 4-6 quarters is realistic for businesses committing to the structural work, and it compounds thereafter.

Success Calibrators runs the Revenue Recovery program for B2B SaaS operators carrying a Churn Tax exposure they want to reduce. The program runs 12 months and puts 75% of our fees at risk against NRR improvement targets. We open the engagement with a diagnostic phase: Churn Tax exposure quantified by layer, maturity-stage gap identified by dimension, current challenges and opportunities and the 12-month NRR recovery trajectory with segment-specific scenarios.

The 2026 NRR conversation has moved away from 120%. Reset the benchmark to 108%, overlay your Churn Tax exposure, and the board narrative aligns to a credible baseline. The Revenue Recovery program operationalizes the rebuild from there.